Why you should NOT Cancel Insurance on your Motorcycle, Boat or Golf Cart in the Off-Season12/26/2016 A lot of vehicles only have seasonal use. This is particularly true for people that live in the northern states. People store their motorcycles, boats and golf carts in the winter, and snowmobile owners store their sleds in the summer. So while your vehicle is not being used in the off-season, there's no reason to keep insurance on it, right???? WRONG! Many people decide to cancel their insurance policies on those vehicles in the off-season. However, there are some major downsides to doing that. This became very clear to me just this past Friday, when a friend that I went to school with had his motorcycle stolen.... Just two days before Christmas, a thief broke into his garage, and stole his 2001 Harley-Davidson Road King classic. This is a very nice bike! Here is a pic, in case any of you happen to see it riding around somewhere....  My friend told me that prior to his bike being stolen, he had considered canceling his policy during the winter months. Thankfully, he decided that what little money he would've saved wouldn't be worth it. So he decided to continue his coverage for the entire year. This included the comprehensive coverage he was carrying, which is what covers vehicles in case of theft. This is the question that owners of seasonal vehicles face. Should you keep coverage on vehicles that you're not currently using? What are the pros and cons as far as risk? How much do you save if you cancel coverage in the off-season? These are just some of the questions that go into the thought process of making that decision. Two schools of thought: 1. Keep coverage the same for the entire year. Pros:

2. Cancel coverage completely during the off-season. Pro:

Great News: There is a better solution than the two options above! Option 3: Adjusting coverage for the off-season When your vehicle is stored in the off-season, Comprehensive coverage is the only coverage you need. So why not keep your policy active and simply drop or lower unneeded coverages? The following coverages only apply during the in-season, when you're using the vehicle:

*** NOTE: Some of you may carry additional coverage on accessories. If so, you'll need to check with your insurance company about dropping collision coverage, and whether that affects accessory coverage. Other points about the Adjusting Coverages option:

Summary:

I hope this gives you a better idea of how to protect your toys during the months not being used, but still save you money by adjusting coverages that are not needed in the off-season. If you live in Ohio, Michigan, Indiana, Pennsylvania, Virginia or West Virginia, and would like an online quote on your toy, I would be happy to help you. Simply click on the link below that you would like a quote on. And as always, I handle all quotes personally and privately. Get a Motorcycle Insurance Quote Get a Boat Insurance Quote Get a Golf Cart Insurance Quote Call me for a Quote

0 Comments

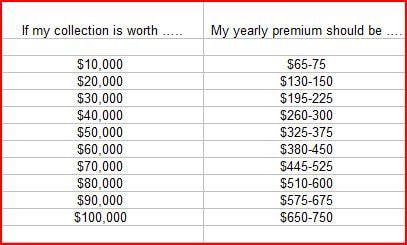

Nearly everyone has their own hobby of collecting things. For some of you that collection may hold quite a lot of value. Do you have the right insurance coverage on those items? And are you paying a fair price for it? By right coverage, I mean insuring for the full value. Many collectible insurance policies do not insure for the full value..... And by fair price, I mean a yearly premium of less than 1% of the insured value. That's what a good collectible insurance policy will do for you. But too many people insure their collectibles with inadequate coverage and/or they pay much more than they should be paying. This article will inform you of what you need to know about collectible items and how to properly insure them for a low price. If you're not getting the full value for your collectibles, or paying more than 1% and yearly premium for the total value of your collectibles, then you need to take a close look at what else is out there. Components of a good Collectibles Insurance Policy

A good Collectibles Insurance Policy is offered at the right price. If you're yearly premium is more than 1 per cent of the value you have insured, you're paying too much! A good collectibe insurance policy normally has premiums less than 1%..... To give you an estimate of costs, see table below....  What is covered:  What is NOT Covered:

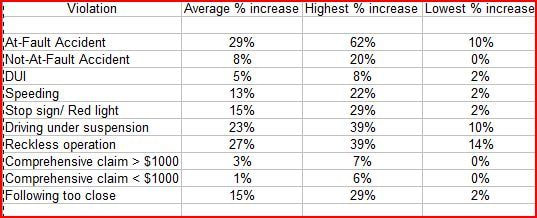

SUMMARY: If your collectibles insurance policy doesn't meet the 3 components of a good policy as described above, you should strongly consider a stand alone collectibles insurance policy that does. If you live in Ohio, Indiana, Michigan, Pennsylvania, Virginia or West Virginia, I may be able to help you. Get a collectibles insurance quote with Lyles Insurance Call me for a Quote Related Blog Articles: Video: Tips for Buying Insurance on Sports Memorabilia Video: Buyers guide for Insurance on Figurines & Action Figures Video: Right Way and Wrong Way to Insure your Collectibles There are several major factors that way and to calculate your auto insurance premium. One of those major factors is your driving record. As you probably know, someone with a clean driving record is usually going to pay less for auto insurance versus someone who has accidents or violations on their record. The real question is How much does a violation increase your auto insurance premium? There are many variables that go in to calculating auto insurance rates. There's no way to give a specific one-size-fits-all answer regarding how much a violation affects car insurance premiums. And while there are hundreds if not thousands of different auto insurance companies, and all of them do their own thing when it comes to how they rate violations. In general, most auto insurance companies fall in one of two categories: the first category are the standard/preferred companies. The second category are the nonstandard/high-risk companies. You'll find out that there is a huge difference in how these two categories vary as far as penalizing drivers for having violations on their record. Standard and preferred companies almost always punish drivers more severely for violations than what nonstandard high-risk companies do. "I have a _______ violation on my record. How much will this raise my auto insurance premium?" Knowing that nonstandard companies go easier on violations versus standard companies helps narrow the choices down somewhat. But this is still a tough question to answer..... WHY? ...... Because even with nonstandard companies, there's a lot of variance between each company, and how they treat each violation differently. How much differently? ...... I decided to do some research on that using real-life actual quotes and compare the dollar amount differences between certain violations. I compared how much more that different violations cost on your auto insurance premium versus what it would cost for someone with a clean driving record, with all other things being equal. How the case study was done.

What this data shows

As an example: Let's say that I have a clean record, and I get quoted at $100 per month with all four companies. If I then take that same quote and add an at-fault accident to my record (without changing anything else), the average price between the four companies would be $129. But with that same violation, I could pay as much as $162, or as little as $110. So Here it is.....  Notes about Violations:

How long do violations affect my insurance rate? Some companies go back as far as five years, but other companies only go back three years. The majority of nonstandard companies only go back three years. Many of the companies that go back five years lessen the severity after three years (so it still counts, but doesn't affect your premium as bad). Common violations not listed above I did not include failure to yield or failure to control violations because they're normally accompanied by an at-fault accident, so only the at-fault accident would count against you.... I also didn't include seat belt tickets. Some companies count seat belt tickets, some don't. three of the four companies I used in this case study do not count seat belts. So there wasn't enough data to include it into the study. Conclusions from this case study

If you live in Ohio, Indiana, Michigan, Pennsylvania, Virginia or West Virginia and would like help finding a lower auto insurance rate, click on the link below, and I'll be happy to run a quote for you.... And as always, I handle all quotes personally and privately. Get an Auto Insurance Quote with Lyles Insurance Call me for a Quote Related Blog Articles Video: 13 Deadliest Driving Behaviors Help! A Vin Number mismatch is causing a snag in buying Auto Insurance The Basics of an Auto Insurance Policy: Breakdown of each coverage explained Right Way and Wrong Way to Cancel Auto Insurance Policies when Switching Companies Understanding named operator (non-owner) auto insurance policies and how to get the best rate |

Author

Dan Lyles is an Independent Insurance Agent serving Ohio, Indiana, Michigan, Pennsylvania, Virginia and West Virginia.. Archives

March 2021

Categories

All

|

RSS Feed

RSS Feed